This post will explain Real estate vs stocks returns. Everyone and their uncle appear to have a great but differing viewpoint on whether it deserves investing in property or the stock exchange. With everyone comes a different view on which “hot” market will win huge and be the catalyst of your monetary future. Although everyone has their own opinion, it is essential to base your decisions on realities and not personal experience. I recently entered a discussion with a family member in the realty service who was considering getting out of the stock exchange totally due to their viewed notion that they were making a lesser rate of return. In my financial knowledge and work in the business, I had opposing views; nevertheless, I understood that they were incomplete and possibly prejudiced.

When Should You Invest In Real Estate vs. The Stock Market?

In this article, you can know about Real estate vs stocks returns here are the details below;

I knew that my moms and dads’ generation had done significantly well investing in property in Canada; nevertheless, were previous generations so lucky? What is the outlook for the future? Certainly, we can’t keep seeing the very same returns, given that my entire generation is getting evaluated of the marketplace.

After this discussion, I chose to look for answers to the question myself– is one market much better than the other? And when is either another suitable?

First, I felt it was necessary to look at a historic breakdown of the returns returning a number of generations.

What is the actual rate of return in the stock exchange?

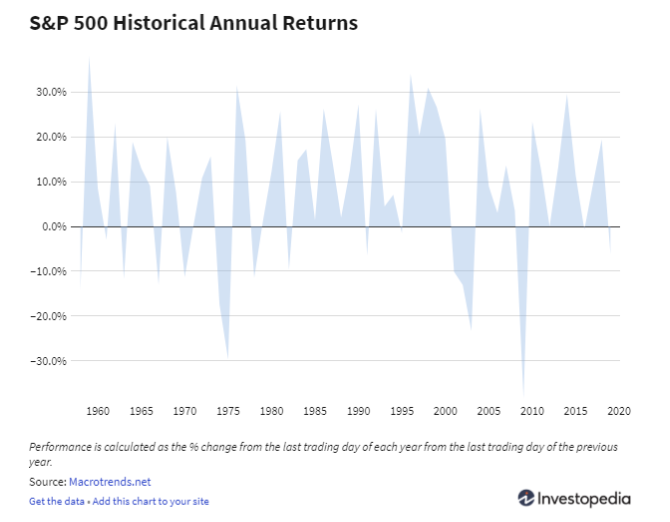

Although there is an infinite quantity of financial investment tools to examine, to get a picture of the total market efficiency, I looked at the annual returns of the S&P 500. The S&P 500 integrates 500 of the US’s largest business– and has considering that 1926. It represents an extensive picture of the stock market and the total economy. Since formation, it has actually returned 7% (adjusted for inflation) typically yearly, and over the last 10 years, it has returned 13.5% every year (consisting of dividends, however not accounting for inflation).

Because no financier can hold stock in the S&P 500, to realize these returns, you require to purchase an exchange-traded fund (ETF) matching the S&P 500. These ETFs follow the holdings of the S&P 500 and try to simulate their returns. If financiers desire their money to carry out at the exact same rate as the market, they can buy these ETFs for a charge called the ‘Management Cost Ratio’ (MER). An instance of such an ETF is the SPDR S&P 500 (ticker SPY) with a MER of 0.09% every year. You subtract this cost from the general returns.

Although these typical returns represent a favourable photo for the stock exchange, it is important to note that a lot of investors don’t recognize these returns completely due to volatility, charges, and insufficient due diligence when selecting financial investments.

What is the historic rate of return in the Canadian realty market?

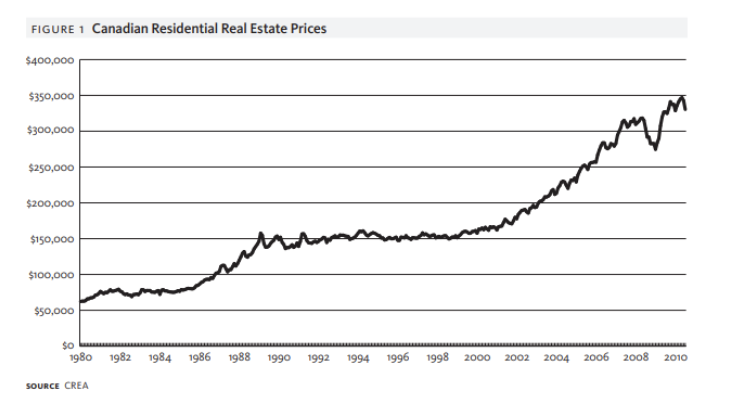

It is no covert trick that Canadian real estate rates have actually soared in the last twenty years. To purchase a home in the Greater Toronto Area in 2019 would get you about $850,000, up 140% from around $350,000 in 2000. This example is similar to my parents’ scenario who purchased our semi-detached household home in main Toronto a little over 20 years ago for $200,000. Its modern value is now over $1.2 M. On the one round, I’m happy that they were able to understand these returns, but on the other, I’m sad remembering that I will suitable not have the ability to raise a household in the city I matured in.

Throughout the nation, appreciating real estate worths were seen over the very same duration, though to a lesser degree, with National housing costs increasing 87% in real terms between 2005 and 2016. That is a boost of 7.25% yearly. These returns are somewhat above the 7% average annual return since beginning of the S&P 500, but less than the production seen over the last 10 years.

These insane property prices were not constantly the case in Canada. As ‘Figure 1– Canadian Residential Real Estate Rates’ shows, prices grew steadily between 1980 to 2000 with two lengthy plateaus throughout the ’80s and ’90s with housing costs equating $75,000 and $150,000. Although that is a 100% improvement over the twenty years, it is still really little compared to the 333% improvement over the last 20 years, with a typical home cost now sitting at $500,000.

What does this data suggest to us today?

From this information, we can conclude that both have actually done likewise effectively over the last 10 years, however I think it would stun individuals to understand that Canadian property returns have actually underperformed the S&P 500.

Psychologically, individuals keep in mind unfavorable events more than positive ones. In other news, losing $100 makes more powerful emotions than acquiring $100. Realty may be viewed more positively due to this phenomenon since, unlike the stock market, you are not able to see the worth of your home fluctuate every day.

I think that both the stock market and realty market serve a function; nevertheless, as a millennial handling impractical housing rates, it’s nice to know that I’m not jeopardizing my financial future by continuing to lease and investing my savings in the stock market.

What are the advantages & drawbacks of each investment chance?

Prior to you invest, it’s important to assess more than just historic returns. As I discussed before, both markets serve a function and assist you reach your financial goals.

Where you select to invest your cash depends on the amount you have, your danger tolerance, whether you require quick path to the money, and the amount of time & energy you are ready to put in.

For a breakdown of these variations, here are the advantages and disadvantages to both alternatives:

Buying the Stock Market

PROS

Capital Requirements: – A considerable advantage to investing in the stock market is how little cash you require to get going. If you have a brokerage statement, you can buy in the stock exchange with as little as $1.00. This is not, however, considering prospective commission charges and administrative charges of holding the account.

Low Upkeep: – If you plan to invest long-lasting with a passive technique, indicating that you aren’t attempting to surpass the market, you can park your cash and not feel it for years until you are available to use it. In addition to being the most convenient method, information programs that a “buy-and-hold” technique is the most favourable for returns.

Strong Historic Efficiency: – Throughout the ups and downs in history, the stock exchange was still able to rebound and offer beneficial typical returns for financiers. Even with the madness of 2020, the S&P 500 is unbelievely just down 0.47% year-to-date. Although historical performance does not equivalent future performance, you can feel great understanding that volatility is only temporary.

Liquidity (Money Accessibility): – You can’t forecast the volatility that might exist at the time of withdrawal, however buying the stock exchange guarantees your money can be made readily offered. For the majority of monetary instruments such as stocks, bonds, mutual funds, and ETFs, you can transform your financial investments into money in two service days.

CONS

Volatility & Danger: – The stock exchange has actually supplied favourable average returns; however, year-over-year gains can be highly volatile. For example, the 2008 monetary crisis caused returns to be -37.22% for the year. Although the marketplaces have actually rebounded considerably, previously this year, we routinely had double-digit drops daily. Due to this volatility, investors need to examine whether they can handle the greater risk and tension compared to other investments.

Taxes: – Although capital gains (the money made from selling a stock higher than the purchase cost) are taxed the most favourably compared to other types of financial investment income such as earnings and interest, there are still tax suggestions. Unless your hold your purchases within a Tax-Free Savings Account (TFSA), the capital gains on your stock financial investments are taxed at 50%.

Investing in the Real Estate Market

PROS

Stability: – As you can inform by the chart, with the small exception of the 2008 financial crisis, the Canadian realty market hasn’t seen a considerable drop in decades. When it pertains to motions in the stock market and economy, the real estate market is generally the last to be impacted, if at all.

Canadian Real Estate Trends: – The upward trends in the real estate market continue to shock financiers. No one can know for positive if these patterns will continue, however current history is definitely on their side.

Accommodation: – A reasonable argument for investing in realty is the fact that everyone needs accommodation. Unless you deal with your parents, you will be paying for it in some type, either through rental payments or mortgage payments. Making monthly payments towards a property in your name sounds much better than paying for your proprietors’ home loan.

Taxes: – Compared to the taxes on capital gains, the gains you make from offering your principal home are tax-free. Canada has a ‘principal home tax exemption’ that permits this if the residential or commercial property was your main home for every single year you owned it.

CONS

Capital Requirements: – Unlike purchasing the stock exchange with as little or as much as you can, buying realty is pricey, and many Canadians might never ever have the monetary means to go into the market According to a 2019 KPMG research study, almost half of millennials feel that owning a home is a “pipedream”.

High Maintenance: – Maintaining home as a landlord or as a homeowner is costly and time-consuming. According to property business UpNest, property owners should expect to pay 4% of the worth of their home every year on upkeep costs. If you own a $500k house, that’s $20k every year.

Liquidity (Cash Ease Of Access): – Property is extremely illiquid as a property, indicating that it’s much more difficult to transform the worth into money, should you ever want it for accidents. For this reason, it’s important to leave any of your cash in other, more easily available types of investment.

What about Property Investment Trusts (REITs)?

I feel that this short article would not be total without touching on the financial investment tool called a REIT. You can see this tool as a combination of the two kinds of properties. Like any other stock, REITs are placed on a stock market for a per-unit purchase rate. They approve people the capability to invest in realty by pooling people’s cash to buy a wide choice of possessions.

There are different REITs for various property residential or commercial properties, such as long-term care facilities, commercial properties, and health care centers, to name a few. Financiers of REITs produce earnings through the arranged circulations. These distributions consist of cash made from capital gains, rent, and other income streams that would be included if you bought home yourself. They are similar to dividends because they are arranged on a month-to-month or regularly basis but are taxed separately depending on the breakdown of how the earnings was made.

PROS.

– You are still bought the realty market.

– Requires little capital to invest

– Low upkeep as you are not a proprietor

– Steady cash flows through the distributions

– Liquidity or easy access to money

CONS.

– Low growth or capital gains opportunity compared to regular stocks

– Circulations are taxed at a greater rate

– Possible for volatility

– Greater management charges

So, is one truly more useful than the other? No. Both have various qualities and can be utilized concurrently to meet your financial objectives. Property ought to not replace your other investments. They can not offer the liquidity, retirement savings opportunities, and tax benefits (if you are buying numerous properties) that monetary investment tools can. Also, contrary to popular belief, they have actually returned more on a typical annualized basis.

This is an essential indicate make as millennials may feel discouraged or pressed to enter the real estate market prematurely. The mental concern of having a home loan you can’t pay for is not worth the perceived advantages. The stock exchange can seem complicated, specifically given this year, however understand that with every downturn in history, the stock market has actually rebounded & returned more for investors. Continuing to pay until you are able while investing your cost savings in the stock exchange, is 1 of the best business decisions you can perform.