This post will explain how to make a budget. If you want to controls your spending and work towards your financial objectives, you need a budget. A personal or home budget plan is a summary that compares and tracks your earnings and costs for a specified period, usually one month.1 while the word “budget” is often connected with restricted spending, a spending plan does not need to be limiting to be efficient.

A spending plan will reveal to you just how much cash you anticipate to generate, then compare that to your needed costs such as rent and insurance and your discretionary spending, such as home entertainment or eating in restaurants. Instead of viewing a budget plan as unfavorable, you can see it as a tool for attaining your financial objectives.

How To Make A Personal Budget In 6 Easy Steps

In this article, you can know about how to make a budget here are the details below;

What a Budget Does

A composed, month-to-month budget is a monetary planning tool that enables you to plan just how much you will spend or conserve monthly. It likewise enables you to track your spending practices.

Though making a budget may not sounds like the most exciting activity (and for some, it’s downright frightening), it’s a vital part of keeping your financial home in order. That’s since budgets count on balance. If you invest less in one location, you can spend more in another, conserve that money for a big purchase, build a “rainy day” fund, increase your savings, or invest in structured wealth.

A budget just works if you are honest about your income and costs. To make an effective budget, you need to deal with detailed and precise info about your earning and costs habits.

Eventually, the outcome of your new budget plan will reveal to you where your money is getting from, how much is there, and where it all goes every month.

How to Make a Budget in 6 Simple Steps

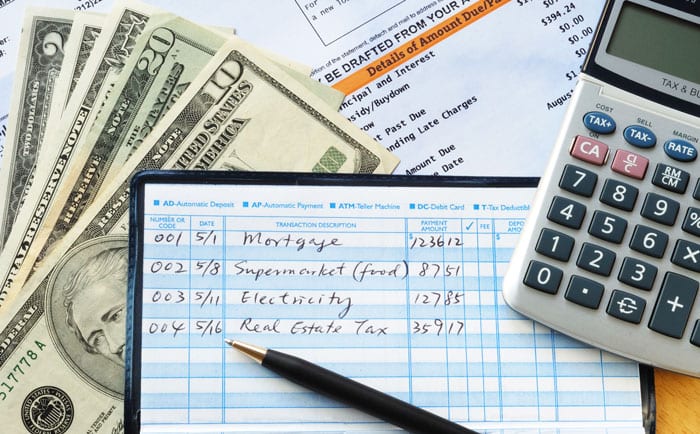

Before you start making a budget plan, discover an excellent design template you can utilize to fill out the numbers for your expenditures and income.

While you can utilize old-fashioned pen and paper to spending plan your cash, it’s much easier and more effective to use a regular monthly spending plan spreadsheet or a budgeting app. These will include designated fields for earnings and costs in various classifications, along with integrated solutions to assist you figure your budget surplus or shortfall with very little effort.

1. Gather Your Financial Paperwork

Before you begin, gather all your financial statements, including:

– Bank statements

– Investment accounts

– Recent energy costs

– W-2s and paystubs

– 1099s.

– Credit card bills.

– Receipts from the last three months.

– Mortgage or automobile loan declarations.

You wish to have access to any info about your income and costs. Among the secrets to the budget-making procedure is to produce a regular monthly average. The more items you can collect, the better.

2. Compute Your Income.

How much income can you anticipate each month? If your earnings are in a regular income where taxes are instantly subtracted, then using the earnings (or net earnings) amount is great. If you are self-employed or have outsides sources of income, such as child support or Socials Security, include these too. Tape these total earnings as a regular monthly amount.

If you have variable earnings (for example, from a seasonal or independent task), consider utilizing the income from your lowest-earning month in the prior year as your baseline earnings when you established your budget.

3. Develop a List of Monthly Expenses.

Document a list of all the expenditures you expect to have during a month. This list might include:.

– Mortgage payments or lease.

– Car payments.

– Insurance.

– Groceries.

– Utilities.

– Entertainment.

– Personal care.

– Eating out.

– Childcare.

– Transportation expenses.

– Travel.

– Student loans.

– Savings.

Utilize your bank declarations, invoices, and charge card declarations from the last three months to identify all your spending.

4. Identify Fixed and Variable Expenses.

Fixed expenditures are those obligatory costs that you pay the same quantity for each time.2 Include items like mortgage or lease payments, cars and truck payments, set-fee web service, trash pickup, and regular childcare. If you pay a basic credit card payment, include that amount and any other necessary spending that tends to remain the very same from month to month.

If you plan to save a fixed quantity or pay off a particular quantity of debt every month, likewise consist of savings and debt repayment as repaired costs.

Variable expenditures are the type that will change from month to month, such as.

– Groceries.

– Gasoline.

– Entertainment.

– Eating out.

– Gifts3.

If you do not have an crisis fund, it consists of classification for “surprise expenditures” that might pop up over the month and thwart your spending plan.

Start appointing spending worth to each category, starting with your fixed costs. Then, approximate just how much you’ll need to spend per month on variable expenses.

If you’re not exactly sure just how much you spend in each classification, evaluate your last two or three months of charge card or bank deals to make a rough estimate.

5. Total Your Monthly Income and Expenses.

If your earnings are more important than your expenditures, you are off to a good start. This extra money mean’s you can put funds towards area’s of your budget plan, such as retirement cost savings or settling a debt.

If you have more earnings than expenses, think about embracing the “50-30-20” budgeting viewpoint. In a 50-30-20 spending plan, “needs,” or necessary costs, need to represent half of your budget plan, should comprise another 30%, and cost savings and debt repayment ought to comprise the final 20% of your budget.

If your costs are more than your income, that implies you are overspending and require to make some changes.

6. Make Adjustments to Expenses.

If you’re in a situation where costs are higher than earnings, discover areas in your variable expenditures you can cut. Look for locations you can reduce your costs– like eating out less– or remove a classification– like canceling your gym subscription.

If your expenditures are far above your income or have substantial debt, reducing your variable expenditures may not suffice. You may require to trim your fixed costs and increase your earnings to stabilize your budget.

Goal to have your income and cost columns to be equivalent. This equivalent balance means all of your income is represented and allocated towards a specific cost or cost savings goal.

How to Use Your Budget.

After you have set up your budget plan, you should keep track of and continue to track your expenditures in each classification, ideally every day of the month. The same budgeting spreadsheet or app utilized to make your budget can also be utilized to tape-record your expense and earnings totals.

Recording what you spends throughout the month will keep you from spending beyond your means and help you determine unneeded costs or troublesome spending patterns. Take a few minutes every day to tape-record your costs, rather than putting it off up until the completion of the month.

If you are not confident that you can budget plan your cash, adopt the envelope system to divide cash for costs into separate envelopes for various costs classifications. When an envelope ends up being empty, you’ll have to stop spending because of the specific category.

As you utilize your budget, watch on how much you have spent. When you have reached your spending limit in a category, you will either need to stop that kind of costs for the month or move cash from another category to cover extra costs.

Your goal in using your funds should be to keeps your expenses equal to or lower than your earnings for the month.

Budgeting Tips.

When you have established a basic budget, personalize it according to your financial circumstance and goals.

1. If you work on commission, be aggressives in saving to assist cover periods when the market is slow.

2. If you have cash flow issues since you are paid only as soon as a month, break that payment by weeks, and keep the money you prepared to invest in the remaining weeks in a different account till you require it.

3. Pay with a credit card just if you will have the money to pay it off at the end of the month. Unless, you will owe interest on top of the cost of whatever you bought.

4. Change your budget plan monthly if you find you overstated or ignored your expenditures. Watch on big expenses that just happen every few months, such as insurance coverage payments.

5. If you tend to spend too much in certain classifications, utilize budgeting hacks to switch to a cash-only budget.

6. As soon as your expenses are lower than your income, budget towards savings objectives before you increase your costs.

7. Take time to learn other monetary skills to improve your monetary literacy and make your money work harder for you.